PSA Market Opportunity Assessment | Healthcare & Consumer Goods

Report Overview:

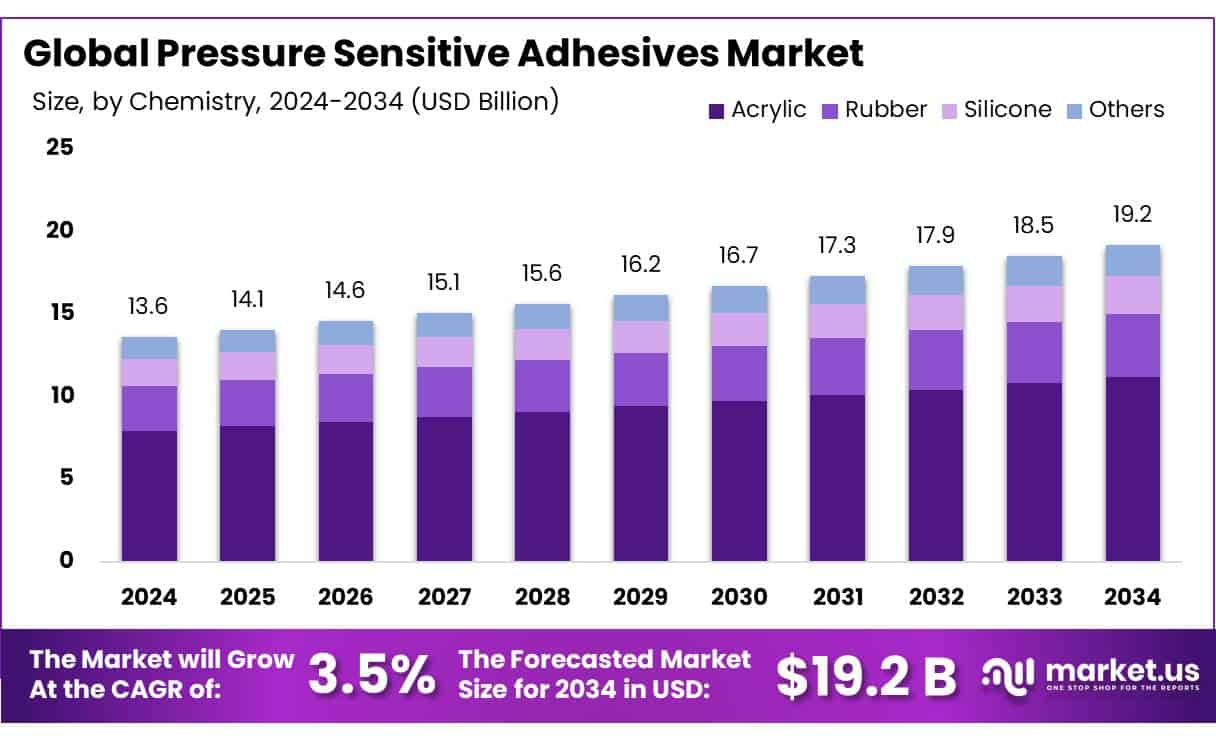

The global pressure sensitive adhesives market is projected to grow from USD 13.6 billion in 2024 to approximately USD 19.2 billion by 2034, reflecting a compound annual growth rate (CAGR) of 3.5% during the forecast period from 2025 to 2034. This steady growth is driven by rising demand across packaging, automotive, healthcare, and electronics sectors due to the versatility and ease of application these adhesives offer.

Water-based PSA formulations currently lead the market, accounting for nearly 47% of the total in 2024. Their clean, low-VOC (volatile organic compound) profile aligns well with global environmental regulations, making them the preferred choice in packaging and labeling. Acrylic chemistry also dominates, offering durability, UV resistance, and versatility across multiple applications, holding nearly 58% market share. PSAs are gaining prominence because they stick under light pressure and don’t require heat or solvents, making them industrial and consumer favorites. They are used in labels, tapes, graphic films, and construction materials, making them versatile and cost-effective solutions.

Key Takeaways:

- The global Pressure Sensitive Adhesives Market is projected to reach USD 19.2 billion by 2034, growing at a CAGR of 3.5% from 2025 to 2034.

- Acrylic-based PSAs dominated with 58.3% market share in 2024 due to their durability, UV resistance, and versatility across industries.

- Water-based PSAs led with a 46.8% share in 2024, favored for being eco-friendly, low-VOC, and compliant with strict environmental regulations.

- Plastic substrates held the largest share, 35.6% in 2024, due to their widespread use in packaging, automotive, and electronics.

- Labels were the top PSA application, capturing 45.9% market share in 2024, driven by demand in food & beverage, pharmaceuticals, and logistics.

- The automotive sector was the leading end-user, holding 42.7% share in 2024, due to demand for lightweight and durable bonding solutions.

- APAC is the dominant region, accounting for 46.3% of the global PSA market USD 6.2 billion, led by China, Japan, India, and South Korea.

Download Exclusive Sample Of This Premium Report:

https://market.us/report/global-pressure-sensitive-adhesives-market/free-sample/

Key Market Segments:

By Chemistry

- Acrylic

- Pure Acrylic

- Modified Acrylic

- Rubber

- Natural

- Synthetic

- Silicone

- Others

By Technology

- Water-based

- Solvent-based

- Hot Melt

- Radiation-Cured

By Substrate

- Plastic

- Paper

- Metal

- Glass

- Wood

- Others

By Application

- Labels

- Tapes

- Single-Faced

- Double-Faced

- Others

- Graphics

- Others

By End-Use

- Automotive and Transportation

- Electronics

- Consumer Goods

- Packaging

- Building and Construction

- Medical and Healthcare

- Others

Drivers

The global pressure sensitive adhesives market is being strongly driven by the growing demand across multiple industries especially in packaging, automotive, electronics, and healthcare. As consumer behavior shifts toward fast delivery and e-commerce convenience, the need for quick, reliable sealing and labeling solutions has surged. PSAs play a critical role in this process, as they bond instantly under light pressure without requiring heat or water, making them ideal for high-speed manufacturing lines and consumer products.

One of the most notable growth factors is the global push for eco-friendly solutions. Governments and regulatory bodies across North America, Europe, and parts of Asia are enforcing stricter guidelines to limit volatile organic compounds (VOCs) in industrial products. PSAs especially water-based and solvent-free variants fit well into this green transition. With their low environmental impact and compliance with sustainability norms, these adhesives are increasingly replacing solvent-based alternatives. Additionally, PSAs offer flexibility and cost efficiency in diverse applications, from automotive trims and protective films to medical tapes and hygiene products. As product designs become more compact and intricate, pressure-sensitive adhesives offer seamless, lightweight bonding solutions that are easy to apply, reposition, and remove.

Restraining Factors

Despite its growing importance, the PSA market faces some challenges that could hinder its full potential. The most pressing is raw material price volatility. The cost of core components like acrylic polymers, natural rubber, and specialty resins can fluctuate sharply based on global supply conditions and crude oil prices. These cost pressures can impact profit margins, especially for smaller producers and suppliers in price-sensitive markets.

Technical performance issues also present a concern. While PSAs are known for their ease of use, they must perform consistently across various temperatures, humidity levels, and substrate materials. Ensuring strong adhesion without leaving residue or damaging surfaces is a constant R&D focus particularly in automotive and medical applications, where performance cannot be compromised. Furthermore, the complex regulatory landscape can be a hurdle. Manufacturers must ensure compliance with environmental, safety, and industry-specific standards across different countries. Adapting to these rules, especially in developing regions with evolving frameworks, can slow down product rollouts and increase development costs.

Opportunities

The PSA market holds tremendous potential in emerging applications and regions. One of the most promising areas is bio-based adhesives. As industries aim to cut down their carbon footprint, adhesives made from renewable feedstocks such as natural rubber, starch, or cellulose are gaining attention. These formulations not only reduce reliance on petrochemicals but also offer improved biodegradability, aligning well with consumer expectations and corporate ESG goals. Digitally printed labels and smart packaging are also opening doors.

Pressure sensitive adhesives that work well with high-resolution printing and digital customization are in high demand. Sectors such as pharmaceuticals and logistics are adopting PSAs in security labels, tamper-evident packaging, and track-and-trace systems, where adhesive quality plays a critical role in functionality. Healthcare is another untapped goldmine. The global rise in chronic diseases and post-operative care has triggered demand for high-performance medical adhesives, used in wound dressings, wearable monitors, and surgical tapes. PSAs that are skin-friendly, breathable, and hypoallergenic are increasingly needed in this growing field. Geographically, regions like Southeast Asia, Latin America, and parts of the Middle East are experiencing rapid infrastructure and retail growth. With better access to modern consumer goods, the need for advanced packaging and labeling is accelerating making these regions key targets for PSA manufacturers.

Trends

Several strong trends are shaping the future of the PSA market. One of the most impactful is the shift toward water-based and solvent-free formulations. These adhesives emit fewer harmful substances and align with global sustainability goals, making them preferred choices for both manufacturers and regulators. Water-based PSAs are particularly popular in the packaging and hygiene sectors due to their safety and low odor. In terms of products, tapes remain the leading application, used extensively in industrial assembly, construction, and packaging. As production automation increases, more industries are switching from traditional fastening methods to adhesive tapes that simplify processes and reduce material waste.

There is also a move toward multi-functionality. Adhesives are no longer just “stickers” they now carry active properties like electrical insulation, UV resistance, thermal conductivity, and biodegradability. These characteristics allow PSAs to be integrated into high-tech fields like electronics, wearables, and green building materials. Lastly, Asia-Pacific continues to dominate the global PSA market, driven by strong manufacturing growth, especially in China and India. This region not only consumes a large portion of adhesives but is also becoming a hub for innovation and production.

Market Key Players:

- Henkel AG and Co. KGaA

- H.B. Fuller Company

- Arkema

- 3M

- Sika AG

- Ashland, Inc.

- Pidilite Industries Ltd.

- Momentive Performance Materials, Inc.

- Franklin International, Inc.

- DuPont de Nemours, Inc.

- Helmitin Adhesives

- DIC Corporation

- Avery Dennison Corporation

- Wacker Chemie AG

- Tesa SE

- Illinois Tool Works Inc

- Scapa

- Jowat SE

- Exxon Mobil Corporation

Conclusion

The global pressure sensitive adhesives (PSA) market is on a stable path of growth, supported by increasing demand across packaging, automotive, electronics, healthcare, and industrial applications. The ability of PSAs to bond surfaces instantly without the need for heat or water makes them highly suitable for fast-paced manufacturing environments. With industries pushing for speed, precision, and lightweight solutions, PSAs offer an efficient and flexible option that meets these evolving requirements.

Environmental awareness is also influencing market dynamics. As regulations become stricter regarding emissions and sustainability, the market is shifting towards water-based and solvent-free adhesives. This transition not only helps manufacturers meet environmental standards but also aligns with the global trend toward greener production. Water-based PSAs, in particular, are gaining popularity in the packaging and hygiene sectors due to their safety, low VOC content, and performance on sensitive materials.

Comments

0 comment