Report Overview:

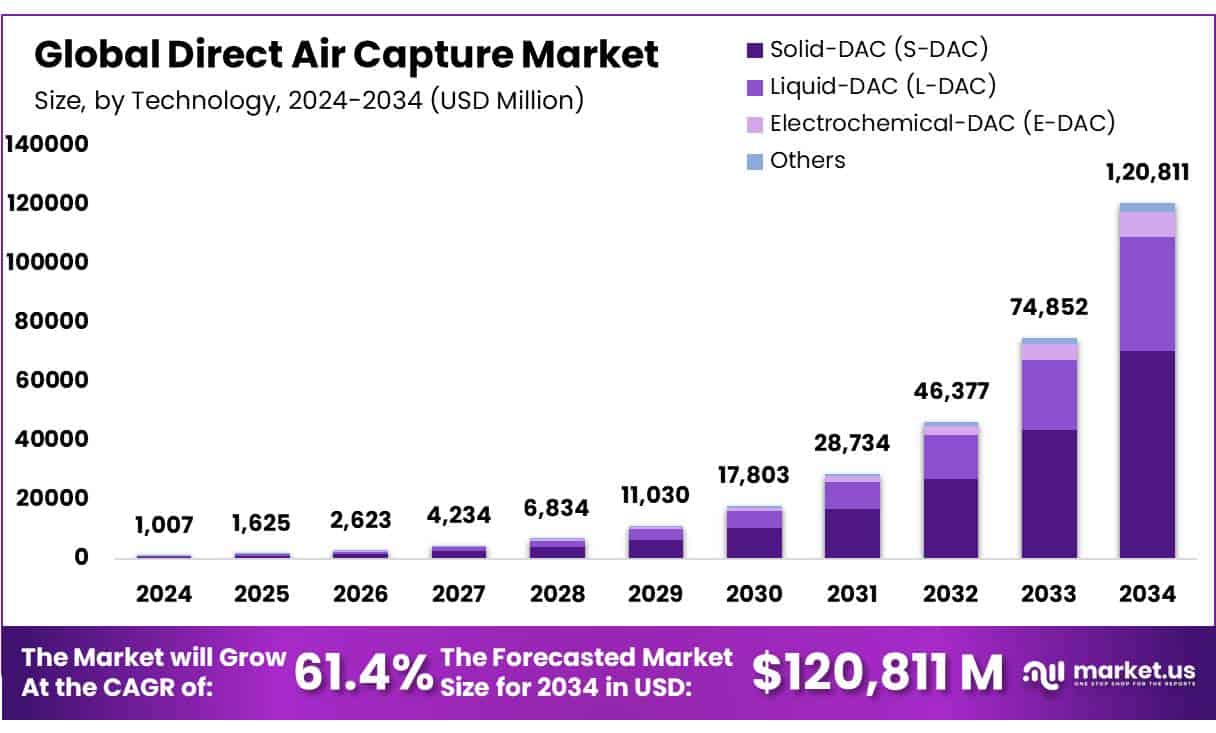

The global Direct Air Capture market reached approximately USD 1.007 billion in 2024 and is on a rapid growth trajectory. Analysts project it soaring to around USD 120.8 billion by 2034, with a compound annual growth rate CAGR of about 61.4%.

DAC technology works by pulling CO₂ directly from the ambient air. Once captured, the CO₂ can either be securely stored underground or repurposed for industrial uses like synthetic fuels, chemicals, construction materials, or beverage carbonation.

The flexibility makes DAC particularly valuable for industries with hard-to-eliminate emissions, such as aviation and agriculture. An array of policy incentives such as tax credits and government funding paired with growing corporate commitments to high-integrity carbon removal, are fast-tracking deployment and investment in DAC.

Key Takeaways:

- The global direct air capture market was valued at US$ 1,007.1 million in 2024.

- The global direct air capture market is projected to grow at a CAGR of 61.4 % and is estimated to reach US$ 120,811 million by 2034.

- Among technology, Solid-DAC (S-DAC) accounted for the largest market share of 58.3%.

- Among energy sources, electricity accounted for the majority of the market share at 68.3%.

- By number of collectors, less than 10 collectors accounted for the largest market share of 46.4%.

- By application, Carbon Capture, and Storage (CCS) accounted for the majority of the market share at 82.1%.

- Among end-use, oil & gas accounted for the largest market share of 34.5%

- North America is estimated as the largest market for direct air capture with a share of 48.3% of the market share.

Download Exclusive Sample Of This Premium Report:

https://market.us/report/direct-air-capture-market/free-sample/

Key Market Segments:

By Technology

- Solid-DAC (S-DAC)

- Liquid-DAC (L-DAC)

- Electrochemical-DAC (E-DAC)

- Others

By Energy Source

- Electricity

- Heat

By Number of Collectors

- Less than 10 collectors

- More than 10 collectors

By Application

- Carbon Capture, and Storage (CCS)

- Carbon Capture Utilization and Storage (CCUS)

By End-Use

- Oil & Gas

- Food and beverage

- Automotive

- Chemicals

- Healthcare

- Others

Drivers:

One of the major driving forces behind the Direct Air Capture market is the urgent global demand for climate solutions that can reduce existing carbon dioxide from the atmosphere. Traditional decarbonization methods, like renewable energy and efficiency upgrades, focus on avoiding emissions.

DAC addresses the accumulated CO₂ already in the air making it a crucial tool for achieving net-zero targets. Governments, especially in North America and Europe, are supporting DAC through favorable policies, grants, and tax credits. These include initiatives like carbon removal mandates, funding for DAC hubs, and direct investment into R&D. As regulatory pressures increase and global agreements tighten emissions limits, demand for DAC is expected to grow rapidly across industries.

Another strong driver is the private sector’s push toward sustainability and carbon neutrality. Companies, especially in hard-to-abate industries like aviation, cement, and oil and gas, are turning to DAC to offset emissions they cannot eliminate. Moreover, investors are increasingly allocating capital to clean tech solutions, including carbon removal technologies.

Opportunities:

The DAC market presents immense opportunities as global awareness of carbon removal intensifies. One of the most promising aspects is the shift toward large-scale deployment of modular, solid-sorbent systems. These systems allow for easier scaling, lower maintenance, and reduced land usage.

As more plants are developed and operating hours increase, economies of scale are expected to lower the per-ton cost of carbon capture. Today’s estimates for some pilot plants exceed USD 600-1,000 per ton, but future projections aim for costs below USD 100-300 per ton. If this happens, DAC could become a commercially viable method of carbon removal across sectors including energy, transport, and heavy industry.

Additionally, captured CO₂ has commercial uses in producing synthetic fuels, chemicals, or construction materials, which opens up new revenue streams. Governments offering carbon credits or “advanced market commitments” for verified CO₂ removal further enhance the commercial appeal. These developments suggest a ripe market environment for technological partnerships, investor interest, and public-private collaboration in scaling the DAC ecosystem.

Restraints:

Despite its potential, DAC technology comes with significant risks that could hinder its large-scale adoption. The biggest challenge is the high cost of capturing and storing carbon from ambient air. Since CO₂ in the atmosphere exists in low concentrations, it requires more energy and technology to isolate and capture it than emissions from industrial stacks or natural gas processing. This makes DAC more expensive than many other climate solutions.

In addition, current infrastructure is limited, with only a handful of plants in operation globally. These high capital costs and limited output create uncertainty for investors and policymakers looking for cost-effective mitigation tools.

There’s also a risk of overreliance on DAC as a climate strategy. Some critics argue that promoting carbon removal technologies might divert attention from emission reduction efforts, especially if industries or governments view DAC as a “get-out-of-jail-free card.” Regulatory frameworks around DAC are still evolving, and the voluntary carbon market which provides funding for removal projects lacks global standardization.

Trends:

One of the most exciting trends shaping the DAC market is the increasing modularization and industrial scaling of carbon capture facilities. Earlier DAC systems were lab-based or pilot projects capturing just a few hundred tons of CO₂ annually. Now, companies and governments are targeting multi-thousand-ton plants, with some aiming to reach capacities of 500,000 to over 1 million tons per year in the next decade.

Modular units make it possible to replicate designs quickly, reduce construction time, and cut costs. These developments indicate a shift from experimental technologies to serious infrastructure investments that can make a measurable climate impact.

Another major trend is the integration of DAC with clean energy systems and value-added CO₂ applications. By pairing DAC with solar or wind energy, operators are reducing lifecycle emissions and boosting environmental credibility. Captured CO₂ is increasingly being seen not just as a waste product but as a valuable input. It’s being reused to produce synthetic fuels, beverages, polymers, and even concrete.

Market Key Players:

- Avnos, Inc.

- Capture6

- Carbon Capture Inc.

- Carbon Collect Limited

- Carbon Engineering ULC

- Carbyon

- Global Thermostat

- Heirloom Carbon Technologies

- Immaterial

- Infinitree LLC

- Mission Zero Technologies

- Mosaic Materials Inc.

- Noya PBC

- Octavia carbon

- RepAir Carbon

- Skytree

- Soletair Power

- Southern Green Gas Limited

- Spiritus

- Sustaera Inc.

- Climeworks AG

- Carbon Xtract Corporation

- Other Key Players

Conclusion

DAC technologies, powered mainly by renewable electricity, lead the charge, further supported by strong North American market share and trailblazing policy frameworks. The dominance of small-scale pilot installations, resulting in elevated costs, highlights the early-stage nature of this industry. Yet with significant public-private investment, innovation in modular design, and renewable system integration, DAC is marching steadily toward cost-competitive, large-scale global deployment.