Hydrocephalus Shunts Market Estimated to Rise with Programmable Valves

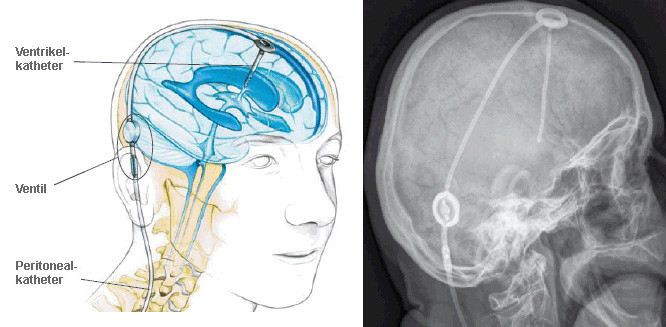

The global hydrocephalus shunts market comprises medical devices designed to divert excess cerebrospinal fluid (CSF) from the brain’s ventricles to other body cavities, thereby reducing intracranial pressure and preventing neurological damage. Core components—ventricular catheters, precise valve mechanisms, and distal catheters—are engineered for reliable long-term performance. Programmable valves and anti-siphon features represent the latest technological advancement, enabling clinicians to non-invasively adjust drainage pressure according to individual patient needs and minimizing risks of over-drainage. Improved biocompatible materials and refined catheter coatings have decreased infection rates and extended device longevity, reducing the frequency of revision surgeries and associated healthcare costs.

The urgent need for effective Hydrocephalus Shunts Market solutions is propelled by rising incidence rates of congenital and normal pressure hydrocephalus in both pediatric and geriatric populations, alongside growing awareness of CSF disorders among healthcare providers. Ongoing collaborations between academic research centers and industry players are accelerating the development of next-generation shunt systems, while detailed market research and market insights inform strategic product launches. This convergence of innovation and clinical demand is reinforcing positive market dynamics and illuminating emerging market segments.

The hydrocephalus shunts market is estimated to be valued at USD 371.4 Mn in 2025 and is expected to reach USD 543.9 Mn by 2032, growing at a compound annual growth rate (CAGR) of 5.6% from 2025 to 2032.

Key Takeaways

Key players operating in the Hydrocephalus Shunts Market are:

-Medtronic plc

-Integra LifeSciences Corporation

-B. Braun Melsungen AG

-Sophysa

-Natus Medical Incorporated

These market companies collectively hold substantial market share and exercise significant influence on global market trends through extensive R&D investments and strategic alliances. Medtronic plc and Integra LifeSciences Corporation lead in product innovation and geographic expansion, driving industry share in North America and Europe. B. Braun Melsungen AG enhances its competitive positioning by broadening its catheter and valve portfolios, while Sophysa leverages licensing agreements to penetrate new territories in Asia Pacific. Natus Medical Incorporated focuses on niche clinical requirements, strengthening its footprint via targeted acquisitions and clinical collaborations. Together, these key players underpin competitive market dynamics and contribute critical market insights that inform future market forecast and business growth strategies.

The Hydrocephalus Shunts Market offers significant market opportunities as healthcare infrastructure expands in emerging economies and governments implement supportive reimbursement policies for early CSF disorder interventions. Rising healthcare expenditure, particularly in Asia Pacific and Latin America, is fueling enhanced access to advanced shunting systems, creating new market segments. Pediatric hydrocephalus management remains an untapped opportunity area, especially in low-and middle-income regions where neonatal screening programs are gaining momentum. Additionally, the aging population in developed markets presents a growing patient pool for normal pressure hydrocephalus treatments. Manufacturers can capitalize on these favorable conditions by forming partnerships with academic institutions to co-develop adaptive and telemetric shunt platforms tailored to regional regulatory requirements. The integration of digital health monitoring and remote patient management tools further amplifies market opportunities, enabling companies to differentiate their offerings and foster sustained business growth.

Programmable valve technology stands out as a key technological advancement reshaping the Hydrocephalus Shunts Market. By allowing non-invasive pressure adjustments post-implantation, programmable valves address persistent market restraints—such as over-drainage complications—and significantly reduce the need for follow-up surgeries. Anti-siphon features complement this innovation by ensuring stable CSF flow regardless of patient posture, enhancing device safety and performance. Moreover, the emergence of telemetric monitoring systems facilitates remote tracking of intracranial pressure dynamics, equipping clinicians with real-time data to optimize treatment plans. This convergence of smart valve platforms and digital health solutions generates comprehensive datasets for predictive analytics, reinforcing market research and supporting evidence-based care. As a result, companies are intensifying their focus on these advanced technologies to secure competitive advantage and drive sustained market growth.

Market Drivers

A primary driver propelling the Hydrocephalus Shunts Market is the escalating prevalence of hydrocephalus diagnoses worldwide, underscored by enhanced imaging technologies and screening protocols. Greater utilization of magnetic resonance imaging (MRI) and computed tomography (CT) scans has led to early detection of CSF accumulation in both neonates and elderly patients. Neonatal screening programs in developed countries are identifying congenital hydrocephalus promptly, while improved awareness among geriatric healthcare providers is increasing normal pressure hydrocephalus diagnoses. Concurrently, rising global healthcare expenditure and shifting emphasis toward value-based care models are encouraging hospitals to adopt advanced programmable shunt systems that lower readmission rates and long-term care costs. Regulatory approvals for next-generation anti-siphon valves and telemetric devices have further stimulated market confidence, enabling faster product launches and broader clinical adoption. Additionally, the backlog of elective neurosurgical procedures post-pandemic has intensified demand for reliable CSF management solutions. The synergistic effect of growing disease incidence, favorable reimbursement frameworks, and continuous technological innovation is expected to sustain robust market growth from 2025 through 2032.

Current Challenges

The hydrocephalus shunts industry grapples with a series of critical market challenges that impede swift innovation and adoption. Regulatory pathways demand extensive market research and rigorous clinical validation before new shunt designs can reach patients, often extending development timelines and driving up costs. Alongside this, tightening reimbursement frameworks in many healthcare systems limit device uptake, even as clinical need grows. Inconsistent coding and coverage policies across regions contribute to complexity for manufacturers and providers, creating fragmentation in treatment accessibility.

Technological sophistication introduces its own hurdles. Designing shunts that balance reliable cerebrospinal fluid regulation with user-friendly implantation requires advanced materials and precision engineering, yet supply chain fragility for key components can stall production. Long-term device durability and patient safety concerns—such as catheter occlusion or infection—remain common market restraints, fueling ongoing clinical investigations and post-market surveillance. Additionally, the capital-intensive nature of R&D places pressure on smaller players, narrowing the field of viable market participants. Collectively, these factors shape the dynamic market dynamics, compelling stakeholders to refine market growth strategies and address both clinical and economic imperatives.

SWOT Analysis

Strength:

The hydrocephalus shunts market benefits from strong clinical traction and growing physician confidence in programmable valve technologies. Continuous advancements in biocompatible coatings and flow-control mechanisms enhance patient outcomes, solidifying industry share in established neurosurgical centers.

Weakness:

• High development and manufacturing costs challenge new entrants, limiting the pool of market players able to invest in next-generation devices.

• Complex post-implant monitoring requirements and specialized training needs for surgeons can slow adoption in smaller or resource-constrained hospitals.

Opportunity:

• Expanding awareness of minimally invasive surgical approaches presents significant market opportunities, as emerging markets seek less invasive treatment alternatives.

• Integration of sensor-based remote monitoring and digital health platforms aligns with broader market trends toward personalized medicine, offering avenues for enhanced patient compliance and competitive differentiation.

Threats:

• Stringent regulatory scrutiny and evolving safety standards may delay product launches and inflate compliance expenses, posing a barrier to timely market entry.

• Growing emphasis on cost containment by payers heightens reimbursement uncertainty, potentially shifting demand toward lower-cost alternatives or off-label uses of existing devices.

Geographical Regions

North America holds a dominant share of hydrocephalus shunts revenue, supported by a robust healthcare infrastructure and high levels of neurosurgical procedure adoption. The United States, in particular, benefits from well-established reimbursement codes and extensive clinical research networks that drive both market insights and demand. Western Europe follows closely, with Germany, France, and the UK leveraging advanced hospital systems and strong academic-industry collaborations to sustain significant market share. These regions also benefit from consolidated distribution channels and comprehensive patient registries, which facilitate post-market surveillance and continuous product improvement—key factors identified in many market reports.

In contrast, the Asia Pacific region is emerging as the fastest growing market segment. Rapidly improving healthcare access, expanding neurosurgical training programs, and increased public–private investment in medical technology underline its accelerating market growth. Countries such as China and India are prioritizing neurological disease management in national health agendas, fueling uptake of modern shunt solutions. Coupled with favorable demographic trends, rising per-capita healthcare expenditure, and nascent reimbursement frameworks, this region offers compelling market forecast optimism. Enhanced local manufacturing initiatives and partnerships between global market companies and regional providers further amplify growth prospects, marking Asia Pacific as a focal point for future expansion.

‣ Get this Report in Japanese Language: 水頭症シャント市場

‣ Get this Report in Korean Language: 수두증션트시장

About Author:

Ravina Pandya, Content Writer, has a strong foothold in the market research industry. She specializes in writing well-researched articles from different industries, including food and beverages, information and technology, healthcare, chemical and materials, etc. (https://www.linkedin.com/in/ravina-pandya-1a3984191)