Carotid Artery Stent Market to Surge with Next-Gen Implant Technology

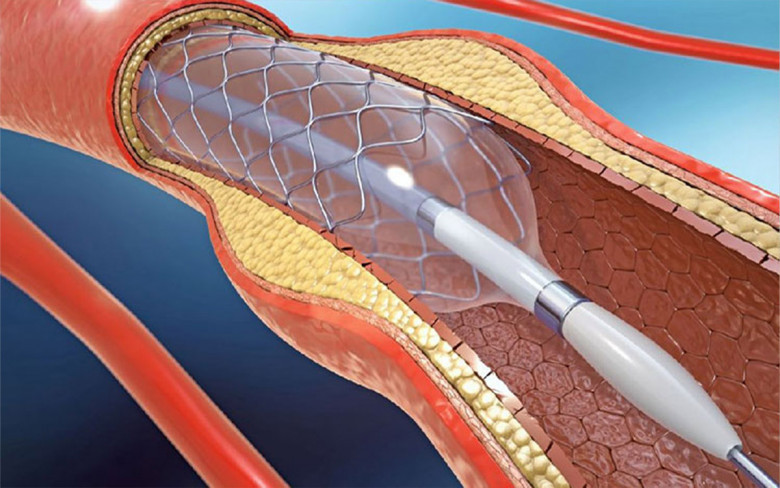

The carotid artery stent market encompasses specialized tubular scaffolds implanted to maintain vessel patency in patients with carotid stenosis, a key factor in preventing ischemic stroke. These stents are typically made of biocompatible metals such as nitinol or cobalt-chromium, offering radial strength, flexibility, and corrosion resistance. Recent product innovations include drug-eluting coatings that inhibit neointimal hyperplasia, as well as next-generation bioresorbable scaffolds that dissolve after vascular healing.

Physicians favor these minimally invasive devices for their ability to reduce procedural time, lower complication rates, and shorten hospital stays compared with open surgery, driving strong Carotid Artery Stent Market demand. Growing awareness of stroke prevention, coupled with improved diagnostic imaging technologies, underscores the need for reliable carotid intervention products. As healthcare providers seek cost-effective solutions, industry share is shifting toward manufacturers that offer comprehensive support programs and evidence-based clinical data.

The carotid artery stent market is estimated to be valued at USD 621.4 Mn in 2025 and is expected to reach USD 817.7 Mn by 2032, growing at a compound annual growth rate (CAGR) of 4.00% from 2025 to 2032.

Key Takeaways

Key players operating in the Carotid Artery Stent Market are:

-Boston Scientific Corporation

-Cordis

-Medtronic

-Terumo Europe NV

-Silk Road Medical Inc.

These market players hold significant market share through broad geographic footprints, extensive distribution networks, and robust product pipelines. Their competitive strategies often focus on mergers and acquisitions to bolster their product portfolios and capitalize on emerging market segments.

Significant market opportunities lie in expanding geriatric populations, rising incidence of atherosclerosis, and growing access to advanced healthcare infrastructure in developing regions. The surge in preventive health screenings and favorable reimbursement policies offer suppliers avenues to broaden market penetration. Strategic partnerships between global market players and regional hospitals promise to unlock new business growth and enhance overall market size, according to recent market research.

Technological advancement in the market centers on next-generation implant technology, including drug-eluting and bioresorbable carotid artery stents. These innovations are reshaping market trends by enabling personalized treatment strategies and reducing long-term complications. Ongoing clinical trials and regulatory approvals are expected to accelerate the adoption of these next-gen implants, driving future market growth and informing comprehensive market analysis.

Market drivers

One of the primary market drivers is the rising prevalence of carotid artery disease, which correlates with an aging global population and an increase in lifestyle-related risk factors such as hypertension, diabetes, and hyperlipidemia. As more patients undergo diagnostic screening via duplex ultrasonography and CT angiography, the detection rate of significant stenosis has surged, fueling demand for carotid stenting procedures. Additionally, the shift toward minimally invasive interventions—driven by benefits like lower perioperative morbidity and reduced hospital stays—has reinforced the demand for advanced stent technologies. Regulatory approvals of next-gen drug-eluting and bioresorbable stents have further enhanced market dynamics, inspiring physicians and healthcare institutions to adopt innovative devices that promise better clinical outcomes. These factors collectively support robust market growth strategies aimed at expanding product availability, improving patient access, and generating higher market revenue over the forecast period.

Current Challenges in the Carotid Artery Stent Industry

The carotid artery stent industry is navigating several critical market challenges as demand for minimally invasive vascular interventions accelerates. One major hurdle stems from stringent regulatory pathways and evolving clinical guidelines, which can delay product approvals and impact market dynamics. Additionally, reimbursement pressures in public and private healthcare systems impose market restraints, forcing manufacturers to adopt cost–efficient production methods while balancing quality and safety. Physicians often favor alternative therapies or open surgical procedures in complex lesion cases, creating resistance to broader stent adoption.

Technological innovation cycles are rapid, and companies must continuously invest in research and development to introduce next-generation drug-eluting or bioresorbable stents. Limited standardization in post-market real-world evidence and varied patient anatomy present further clinical challenges that slow widespread acceptance. Supply chain disruptions—exacerbated by global logistics bottlenecks—also constrain timely delivery of stents to interventional cardiology centers. These factors combined highlight an industry grappling with complex market drivers and evolving market trends, underscoring the need for robust market research and strategic collaborations to address current barriers and capitalize on emerging segments.

SWOT Analysis

Strength:

• Clinically proven efficacy of modern carotid stent designs has improved patient safety and outcomes in stroke prevention, reinforcing physician confidence.

• A diverse range of stent sizing and delivery systems enhances procedural flexibility, supporting penetration into varied anatomical segments.

Weakness:

• High development costs and lengthy regulatory review timelines limit rapid product launches, impeding agility in responding to market demands.

• Dependence on a narrow number of raw material suppliers for specialized alloys creates vulnerability to price volatility and supply interruptions.

Opportunity:

• Growing adoption of drug-eluting and bioresorbable technologies offers a pathway to reduce restenosis rates and capture untapped market opportunities.

• Expansion of minimally invasive treatment guidelines in emerging healthcare systems provides significant room for geographic growth and increased industry share.

Threats:

• Intensifying competition from alternative carotid endarterectomy procedures and non-stent-based therapies threatens to erode stent market share.

• Potential reimbursement cuts and shifting health-economics priorities could undermine revenue forecasts and hinder capital investment.

Geographical Regions with Highest Market Value

North America maintains the largest share of the carotid artery stent market, driven by advanced healthcare infrastructure and high procedural volumes. The United States accounts for a substantial proportion of global industry share, supported by robust clinical adoption and favorable reimbursement policies. Western Europe follows closely, with Germany, France, and the UK leading in interventional cardiology procedures. These regions benefit from well-established market segments in both private and public hospital settings, facilitating steady market growth. Japan also contributes notable value, backed by a growing base of cardiovascular clinics and strong market analysis indicating sustained demand for minimally invasive vascular devices. High per-capita procedure rates and investments in imaging technologies further bolster Asia Pacific markets such as South Korea and Australia. Collectively, these regions represent the core market scope, supported by extensive research centers driving device refinement and evidence-based practice guidelines.

Fastest Growing Region in the Carotid Artery Stent Market

The Asia Pacific region is emerging as the fastest growing market for carotid artery stents, fueled by increasing incidence of cardiovascular diseases and expanding healthcare accessibility. Countries like China and India are witnessing rapid adoption due to government initiatives aimed at improving infrastructure in tier-2 and tier-3 cities. Rising disposable incomes and improved insurance coverage are enhancing patient affordability, underpinning robust market growth. Significant investments in hospital modernization, along with training programs for interventional cardiologists, are accelerating procedural uptake. Moreover, local manufacturers are forging strategic partnerships with global market players to expand distribution networks and introduce cost-effective stent systems tailored to regional patient profiles. Latin America and the Middle East are also demonstrating double-digit expansion rates, driven by concerted efforts to implement comprehensive stroke prevention programs. Overall, these fast-growing regions present lucrative market opportunities for stakeholders aiming to deploy targeted market growth strategies and capture emerging demand.

‣ Get this Report in Japanese Language: 頸動脈ステント市場

‣ Get this Report in Korean Language: 경동맥스텐트시장

About Author:

Ravina Pandya, Content Writer, has a strong foothold in the market research industry. She specializes in writing well-researched articles from different industries, including food and beverages, information and technology, healthcare, chemical and materials, etc. (https://www.linkedin.com/in/ravina-pandya-1a3984191)